Mexico’s Central Bank Governor Says Bitcoin Is Not Money

According to Alejandro Diaz, governor of Mexico’s central bank el Banco de México, Bitcoin is not real money. “Whoever receives Bitcoin in exchange for a good or service, we believe that transaction is more akin to barte...

Archive context

Older archive item. Useful for background and entity history, but not a fresh market-moving signal.

According to Alejandro Diaz, governor of Mexico’s central bank el Banco de México, Bitcoin is not real money.

“Whoever receives Bitcoin in exchange for a good or service, we believe that transaction is more akin to bartering because that person is exchanging a good for a good, but nor really money for a good,” Diaz reportedly said.

“Bitcoin is more like a dimension of precious metals than daily legal tender,” he added.

Bitcoin: a poor store of value?Diaz said that Bitcoin is not a reliable store of value either, taking aim at one of the most popular narratives shared by advocates of the flagship cryptocurrency.

“People will not want their purchasing power, their salary to go up or down 10% from one day to another. You don't want that volatility for purchasing power,” said Diaz. “In that sense, it is not a good safeguard of value.”

In El Salvador—the only country in the world where Bitcoin is legal tender—many citizens would agree with Diaz.

Salvadorans have protested—and protested some more—to prevent the government from adopting the cryptocurrency as legal tender.

Despite the controversy, as well as warnings from international organizations like the World Bank and the IMF, El Salvador’s President Bukele pushed forward, making it the first country in the world to do so.

El Salvador Forced Through Its Bitcoin Law by Any Means NecessaryDuring the first few hours of El Salvador’s Bitcoin project, the cryptocurrency almost immediately plunged by double-digits, adding credence to Diaz’s warnings.

When Bukele announced the purchase of 200 Bitcoin (and revealed the country had already purchased 400 Bitcoin for its reserves) the cryptocurrency was priced close to $53,000. Soon thereafter, Bitcoin fell by more than 10%, resulting in millions of dollars worth of losses in just a few hours.

Bukele—like most other ardent Bitcoiners—reacted by buying the dip. A move that would likely not gain approval if someone asked Mexico’s central bank.

Why this matters

This bitcoin story adds another data point to the current market tape and is useful when read alongside nearby source coverage.

Original source

Read on DecryptRelated market context

Ripple CLO Stuart Alderoty Defends Clarity Act Consumer Safeguards: “Perfect Can’t Be the Enemy of Good”

In a recent post, Alderoty described the Clarity Act as “a consumer protection bill,” pointing to its anti-money laundering and kn...

Poolin, Once-Dominant Bitcoin Mining Giant, Announced Bankruptcy

Key Takeaways: Poolin has filed for Chapter 11 bankruptcy protection in the U.S., representing about 20% of Bitcoin’s global hashr...

The Velocity of Value: How Blockchain is Reshaping Micro-Payments

Blockchain has opened up payment models that were awkward and/or uneconomic under older rails. This is especially true for digital...

DeFi’s next institutional hurdle is deciding who can be trusted to price real-world assets

DTCC now runs a tokenization trial with roughly 40 firms, including JPMorgan, Goldman Sachs, BlackRock, Vanguard and the NYSE, to...

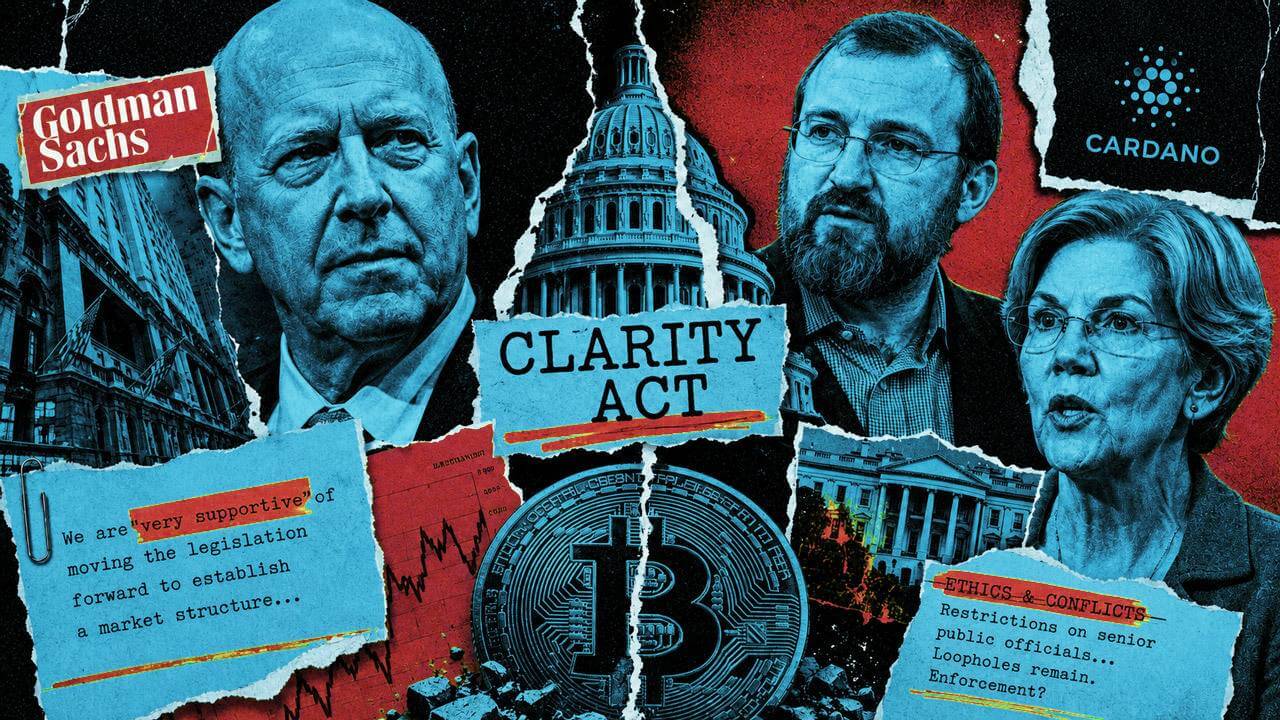

CLARITY Act splits Wall Street and crypto as Goldman Sachs breaks with banks and Charles Hoskinson backs Warren

The revised CLARITY Act is exposing unusual divisions across Wall Street, Washington and the crypto industry as lawmakers struggle...

Bitcoin mining giant Poolin files for bankruptcy owing 11,700 users $164 million

Bitcoin mining pool Poolin Technology filed for Chapter 11 with $163.7 million in IOUs owed to wallet users. Its two Texas affilia...