The Case For Bitcoin In Pakistan

The decentralized, economically empowering technology could bring major benefits to the country.Executive SummaryThis paper is an attempt to highlight Bitcoin’s ever-increasing importance to Pakistan’s socioeconomic futu...

Archive context

Older archive item. Useful for background and entity history, but not a fresh market-moving signal.

The decentralized, economically empowering technology could bring major benefits to the country.

Executive SummaryThis paper is an attempt to highlight Bitcoin’s ever-increasing importance to Pakistan’s socioeconomic future. For purposes of our discussion, Bitcoin refers to the decentralized digital asset with a market capitalization of approximately $900 billion and growing as well as its blockchain-powered monetary network that enables peer-to-peer transactions without relying on a trusted intermediary.

Before we proceed, let us be clear on what this paper will not set out to achieve. Although we are very bullish on bitcoin as an asset class over the long term, our commentary will not include any price forecasts. We will not be conducting a technical review of the blockchain technology in this study. Notwithstanding their importance, these topics have been studied in detail by experts more qualified than our team. Furthermore, a deep dive into a pricing and technical discussion will detract us from the main message: Why should Pakistan adopt bitcoin now?

Cryptocurrency adoption has started to gather momentum in the country. Chainalysis’ 2021 Global Crypto Adoption Index has Pakistan ranked in third place globally. Earlier this year, the province of Khyber Pakhtunkhwa announced plans to build pilot cryptocurrency mining farms. At the federal level, a committee has been formed to study cryptocurrency regulation. These are promising developments. However, there is so much more left to accomplish and a small window of opportunity presents itself to act.

Pakistan has several ways to benefit from the Bitcoin ecosystem. Our team believes bitcoin is primed to outperform traditional assets moving forward. Before the price of bitcoin goes beyond the country’s affordability threshold, we propose the State Bank of Pakistan start by converting up to 5% of their sovereign gold reserves (approximately $180 million) into this asset. The upside scenario can have a positive material impact on the state of the country’s asset reserve balance.

Using the internet and a smartphone, here lies an opportunity for the average Pakistani investor to plug into the world’s best performing asset over the past decade. These unmatched returns will provide prosperity across investing households, boost the local economy in the form of additional demand and generate tax on capital gains. We suggest the State Bank of Pakistan and securities regulator open up access to this asset class for all Pakistani investors. Movement between the Bitcoin ecosystem and traditional financial institutions needs to be a low-cost and frictionless endeavor. A fully regulated national cryptocurrency exchange should be introduced with incentives to entice domestic participation. A bitcoin ETF trading on the Pakistan Stock Exchange will offer an attractive investment for local stock market investors desperate for diversified exposure.

Blockchain and smart contract software developers are on their way to becoming prized assets in this new decade of cryptocurrency. In a post–COVID-19 world, remote work is quickly becoming the new normal. We may not be too far from a future state where the best candidates for the role are recruited, regardless of their physical location. Government investment toward skills upgrade and setting up basic cryptocurrency infrastructure will be returned to the economy in the form of budding entrepreneurs, developers and product managers. All productive citizens would boost the local economy from their earnings and contribute to the tax base. In summary, the cryptocurrency economy has the potential to raise masses out of poverty by providing employment.

The “great mining migration” has presented Pakistan with a time-sensitive investment opportunity. Firstly, the recent reduction in the network’s hash rate makes it economically attractive to begin mining operations immediately. Next, the shutdown of Chinese miners has resulted in secondhand mining equipment flooding the market at considerably reduced prices. Finally, Pakistan now possesses surplus electric generation capacity relative to demand. It is our suggestion that the federal government take advantage of this superb timing. Bitcoin mining farms should be set up near power plants to minimize any transmission losses. If bitcoin prices continue to rise as per our expectations, this is another avenue for the federal government to generate massive revenues.

The State Bank of Pakistan has prioritized the rollout of Raast, a new instant payment system. All evidence points to a flourishing local remittance ecosystem. However, international payment remittance remains a clunky process with high fees and lengthy settlement periods. Bitcoin’s monetary network provides a comprehensive solution to this problem. Specifically, Bitcoin’s Layer 2 protocol (Lighting Network) enables transfer of micropayments on a real-time basis with minimal fees. We suggest the federal committee overseeing cryptocurrency to invite fintech players such as Strike to understand the benefits of this solution. Pakistan should begin work on seamlessly connecting Raast to the Bitcoin ecosystem.

The Bitcoin ecosystem is not without risks. China and the International Monetary Fund (IMF) have both leveled criticism against the technology. Furthermore, the Financial Action Task Force has called on the government to better regulate the cryptocurrency industry. It is imperative to involve these important stakeholders in all top-level cryptocurrency discussions.

Pakistan has multiple avenues available to participate in the Bitcoin revolution. The benefits are far reaching and greatly outweigh the costs. There is an urgency to formulate a national cryptocurrency strategy and become an early adopter of this ecosystem. The time to act is now.

— — — — — — — — — —

I. What Is Bitcoin?The advent of the internet-enabled society to digitize information. In the same vein, bitcoin’s revolutionary technology (the blockchain) enables society to digitize value.

Prior to bitcoin, most cryptocurrencies were exposed to a risk known as double spending. This is the risk that a cryptocurrency can be spent twice. It is a potential problem unique to “digital currencies” because digital information can be reproduced relatively easily by savvy individuals who understand the blockchain network and the computing power necessary to manipulate it (Frankfield, 2020).

Bitcoin was the first cryptocurrency to solve the double spending problem without relying on a central authority to oversee transactions.

Here is an investment letter from Miller Value Income Strategy that provides as simple an explanation of the technology (Bill Miller IV, 2021):

“Bitcoin is a decentralized network of value storage. Its core technological breakthrough lies in users’ ability to transfer value to other network participants without any central administrator or authority. This means that users can shift large quantities of value to each other around the globe almost instantly, 24 hours/day, 365 days/year, using only another participant’s ‘public key’ and little administrative hassle. ‘Miners’ verify transactions in exchange for new coins, though the reward for each mined ‘block’ decreases every 210,000 blocks, or approximately every four years. Unlike the dominant systems of account now in use (currencies), the supply of measuring units is predetermined and will never exceed 21,000,000. While aggregate participation in the network is effectively unlimited, there will never be more than 21 million spots (‘bitcoins’) on the ledger, which means that more network participation makes each spot on the ledger more valuable. Each bitcoin is divisible into 100 million units, or Satoshis.”

The decentralized nature of this technology allows users to conduct peer-to-peer monetary transactions without the need to involve a central authority (i.e., banks, currency exchanges, trust companies, etc.). Bitcoin has rules and incentives built into the protocol that are agreed to and enforced by the miners using a consensus mechanism process. Improvements to the technology can be proposed but can only be adopted if 95% consensus is reached among miners (Alex Galea, 2018). As an example, Taproot, the first Bitcoin upgrade in almost four years, has recently been approved by miners and will take effect in November 2021. However, this ecosystem does not have any rulers. There exists no one person or group that controls Bitcoin. This form of organization where there is no controlling centralized actor is known as distributed governance.

Furthermore, Bitcoin is a permissionless system. As there exists no central authority with ultimate control of the network, any individual or group has the right to transact in this ecosystem using a simple internet connection. A user can neither be banned nor suspended from using the network. No central authority has the right to determine whether a transaction can be conducted on the blockchain.

Another important feature of Bitcoin technology is its immutability. Once a transaction settles on the blockchain, it cannot be edited, reversed or replaced. This ledger of all transactions going back to the very first one from January 2009 can be viewed by anyone on the blockchain. The value of transferred bitcoin, public key addresses of both sender and receiver, along with the date and time of the transaction are all recorded on the blockchain. The high level of confidence in the truth of each transaction brings about a standard of data integrity and transparency that has not been available in the past.

Although bitcoin transaction data is transparent on the blockchain, the parties (i.e., buyer and seller) in each transaction remain anonymous. These buyers and sellers are identified on the blockchain through their unique public keys (a long string of alphanumeric characters). However, all other user-identifying information is not required to transact in this ecosystem. As a result, Bitcoin extends a level of privacy to its users that is not common in the centralized finance world.

Last but not least, bitcoin is referred to as hard currency, in large part, due to its scarcity. The protocol is preprogrammed such that there will exist a total of 21 million bitcoin. So far, roughly 18.8 million bitcoin have been mined and make up the current monetary supply. Furthermore, every four years or so, a halving event takes place. This creates a situation where the number of bitcoin entering the ecosystem reduces by 50% thereby accelerating scarcity. Unlike fiat currency value that is directly tied to the actions of its central bank, bitcoin follows through on its protocol independent of the economic situation around it. This predictability of the protocol is a strength as it ensures the current supply will not be debased due to central bank actions such as excessive money printing.

II. Current State: Cryptocurrency Ecosystem In PakistanThe cryptocurrency boom is upon us. The unprecedented price volatility in this asset class coupled with a relatively low barrier to entry has resulted in a breeding ground for scores of risk takers willing to try their hand at short-term trading. Chainalysis’ 2021 Global Crypto Adoption Index has Pakistan ranked in third place globally, up from 15th place a year before. Specifically, the on-chain retail value transferred metric used to measure the activity of nonprofessional, individual cryptocurrency users ranks Pakistan in the top-10 globally. This ranking underscores the grassroots revolution taking place in the country as more and more Pakistanis enter the cryptocurrency ecosystem.

A. Khyber Pakhtunkhwa

In December 2020, Khyber Pakhtunkhwa provincial assembly unanimously passed the resolution to legalize cryptocurrency and cryptomining (The Express Tribune, 2020).

Soon after, in March 2021, the province of Khyber Pakhtunkhwa announced plans to build pilot cryptocurrency mining farms using hydroelectric power. The provincial government also set up an Advisory Committee on Digital Assets composed of stakeholders and experts with a goal to review various technical matters and associated revenue potential by attracting cryptocurrency-related investments. Zia Ullah Khan Bangash, then advisor to the provincial government on science and technology, sounded upbeat on the future of crypto in the province.

“People have already been approaching us for investment, and we want them to come to Khyber Pakhtunkhwa, earn some money and have the province earn from that as well.

“It’s really just our government that is not participating right now, people all over Pakistan are already working on this, either mining or trading in cryptocurrencies and they are earning an income from it,” Bangash said. “We are hoping to bring this to a government level so things can be controlled and online fraud or other scams can be prevented” (Farooq, March 2021).

However, in a sudden reversal of events, it was announced on May 28, 2021, that the Khyber Pakhtunkhwa government has dissolved the Advisory Committee on Digital Assets citing that decisions on digital currency can only be taken by the federal government. No news has been announced on the cryptocurrency mining farms and associated investments in the province (Ahmed, 2021).

B. Federal

We are of the opinion that the position of the federal authorities, including the State Bank of Pakistan (SBP) on cryptocurrency is not explicit.

Although cryptocurrency itself is not illegal in Pakistan, the on-and-off ramp connecting the ecosystem to traditional financial institutions does not come without headaches. A SBP circular, issued in April 2018, advised “all banks and payment system operators to refrain from processing, trading and promoting in virtual currencies token and not facilitate their account holders to transact in VC and tokens” (Khurshid, 2020). As a result, Pakistani residents are not able to use their bank accounts or online wallets to directly transfer funds to their cryptocurrency exchange accounts.

In order to get around this restriction, most Pakistani cryptocurrency traders and investors use peer-to-peer (P2P) transactions as a method to fund and withdraw from their exchange account. Popular cryptocurrency trading apps provide a listing of verified, country-specific brokers on their platforms. A user looking to fund their cryptocurrency account would send a standard bank transfer to a verified broker’s bank account. The broker would then deposit the agreed-upon cryptocurrency to the user’s exchange account using their public keys address. A withdrawal of funds from the trading app requires a transfer of cryptocurrency from the user to the broker’s exchange account. The broker would then deposit the fiat currency to the user’s bank account using a standard bank transfer. The brokers charge a premium to the market exchange rate for the services provided. The popularity of this P2P process in Pakistan is reflected in the country’s top-10 rank in Chainalysis’ latest P2P Exchange Trade Volume survey. In essence, the P2P process levies an additional cost on Pakistanis transacting in the cryptocurrency ecosystem.

According to recent news reports, a federal committee has been formed to study cryptocurrency regulation. The members are observers from the Financial Action Task Force (FATF), federal ministers, and heads of the country’s intelligence agencies (Farooq, July 2021). This is welcome news and a necessary ingredient in bringing the cryptocurrency revolution to the mainstream economy.

State Bank of Pakistan has also expressed an interest in studying central bank digital currencies (CBDC). In a recent interview with CNN, Governor Reza Baqir cited “financial inclusion, tracking money laundering and counterterrorism measures as possible benefits of digital currencies.” To be clear, CBDC is a digital currency, however, it is under the control of the central bank. This centralized nature makes it distinct from a cryptocurrency such as bitcoin.

The SBP has already started work on Raast, a nationwide instant payment system that will enable end-to-end digital payments among individuals, businesses and government entities within seconds (Ikram, 2021).

This first step in laying down a comprehensive financial rails network is an impressive feat. Our team believes the success of this initiative can lead to on-and-off ramp connections from traditional finance to the cryptocurrency ecosystem.

C. Stacks Education Grant

Earlier in 2021, LUMS, one of Pakistan’s leading universities, was the beneficiary of a research grant earmarked to design Pakistan’s first-ever academic program for blockchain, distributed ledger technology (DLT) and associated platforms.

The grant was in the amount of 5 million STX tokens (a digital currency with an equivalent value of $2.5 million at the time of the announcement). Hiro, the organization behind the grant, builds developer tools for Stacks, the network that enables apps and smart contracts for Bitcoin.

Stacks Pakistan, the local Stacks chapter launched in late 2020, is focusing on awareness, community building and advocacy. The chapter has launched the “Stacks Developers Guild Programme,” or SDG, in seven cities across Pakistan. Through a network of ambassadors, SDG leaders are playing a pivotal role in spreading awareness across universities in Lahore, Karachi, Islamabad, Quetta, Peshawar, Faisalabad and Abbottabad (LUMS, 2021).

III. Bitcoin As A Sovereign ReserveEconomists watched with fascination as the country of El Salvador readied itself to become the global pioneer in accepting bitcoin as legal tender. The Legislative Assembly voted to accept bitcoin as one of two official currencies in the country.

The adoption of bitcoin in the mainstream economy is an interesting case study and not without risks. We feel it is still too early for Pakistan to go the route of accepting bitcoin as an official currency. However, the SBP and Ministry of Finance should pay attention to El Salvador’s rollout. The recently created federal committee should capture the learnings from this public policy experiment, understand the risks and, perhaps, initiate contact with relevant El Salvadoran government officials to remain close to this situation.

An easier way to dip their toes in the cryptocurrency ecosystem would be to consider adding bitcoin to the country’s sovereign reserves. As of July 2021, Pakistan holds $3.795 billion worth of gold reserves (CEIC, 2021).

Gold has been a preferred sovereign reserve asset for most countries going back centuries. There exist two major reasons for this favoritism. First is gold’s globally perceived strength as a store of value. In the event of a fiat currency devaluation or an outright collapse of the local economy, central banks can take refuge in the uncorrelated value of their gold reserves. Finally, gold has a long track record as a valuable global commodity. There are ready buyers available at market prices in the event immediate liquidation is required. For this reason, gold is considered a means of exchange.

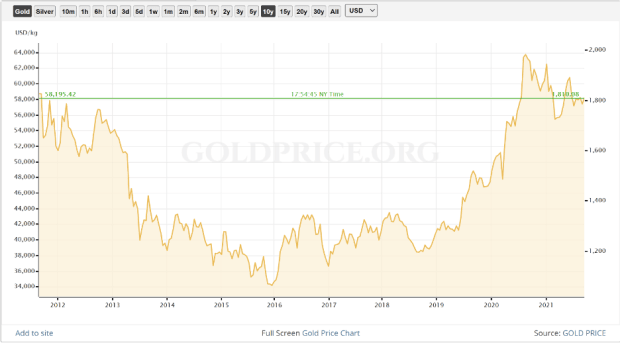

Chart 1.1. Gold Price Performance, 10-year time frame.In order to be classified as a store of value, the asset (or currency) should be worth the same or more in the future. At first glance, the price of gold denominated in USD over a 10-year period seems to have held its value. However, if you account for the 21% cumulative U.S. inflation rate over this time period, the price performance of gold has been abysmal. This data points to gold’s failure as a store of value as it has generated negative real returns (US Inflation Calculator, 2021).

Chart 1.2. Bitcoin Price Performance, 10-year time frame.Conversely, bitcoin has been the best performing asset class over the past decade. Bitcoin generated a compounded annual growth rate of 230% over this time period. As far as store of value goes, you will be hard-pressed to find an asset class better suited than bitcoin.

It is a mathematical impossibility for bitcoin to replicate these returns over the next 10 years. However, our team believes it is primed to outperform traditional asset classes moving forward. The fixed supply of 21 million coins coupled with accelerating scarcity sit at the core of this investment thesis. Moreover, the institutional demand of bitcoin bodes well for future price appreciation and helps to create a price floor. Publicly traded companies in the United States such as Tesla, Square and MicroStrategy have purchased bitcoin as a corporate treasury reserve asset favoring it over the U.S. dollar. Bitcoin exchange traded funds have been approved in Canada and trade on the Toronto Stock Exchange (TSX), thereby creating further retail demand. Even MassMutual has purchased $100 million in bitcoin for its general investment fund.

Chart 1.3. Pakistan’s Gold Reserves, 10-year time framePakistan’s gold reserves weigh roughly 64 tons. The storage and transfer costs for this quantity come with costs. Fortified locations with armed security personnel would not be uncommon. If the gold is stored in bank vaults outside the borders of the country, a management fee is likely paid for this service. In this second scenario, the country’s gold would be in the control of foreign actors. This is not without risks as these foreign powers hold influence on the sale and transfer of these sovereign reserves (World Gold Council, 2021).

Bitcoin has significant advantages over gold when it comes to storage. As bitcoin is a digital asset, it does not require the same level of physical security needed to protect gold reserves. Cold storage and multisignature wallets are examples of bitcoin storage options. In both cases, the costs associated with storage are immaterial. Additionally, the control over the bitcoin rests entirely with the owner of the coins. No central authority can influence the purchase, sale or transfer of these assets. MicroStrategy has created the Bitcoin Corporate Playbook that not only provides guidance on safely storing bitcoin but also how to purchase significant amounts without materially impacting market price (MicroStrategy, n.d.).

Finally, bitcoin is a relatively new asset class with a growing spot and futures market. The bitcoin market has a market capitalization of approximately $950 billion with a three-month average daily traded volume of $32.98 billion (Yahoo Finance, 2021). The market trades round the clock with no days off on weekends or statutory holidays. There exists ample liquidity in the market for Pakistan to consider initiating a small yet calculated position. Furthermore, the daily traded volume points to a ready market of buyers in the event liquidation of position is required. The purchase and sale of this asset is seamless through the use of established global market exchanges. For the amounts in question, bitcoin provides a means of exchange no different than gold.

El Salvador is the first country to make public its adoption of bitcoin as a sovereign asset. We believe more countries will follow suit as they begin to understand the benefits of this digital asset. The current price of bitcoin still falls within Pakistan’s affordability threshold. This may not be the case for too long as adoption increases over time. Therefore, it is vital Pakistan be a first mover among nation states. We propose the State Bank of Pakistan start by converting up to 5% of their gold reserves (i.e., approximately $180 million) to finance their first bitcoin purchase. As it is, these growing gold reserves sit idle and unproductive. Bitcoin satisfies the store of value and means of exchange requirement and offers diversification to the sovereign reserve asset portfolio. We feel this allocation is low enough to not cause panic during price volatility. However, the upside scenario can have a positive material impact on the state of the country’s asset reserve balance.

IV. Poverty AlleviationThe prime minister of Pakistan has highlighted reduction of poverty and the uplift of poor people’s living standards as a major goal of his administration. Launched in 2019, the federally sponsored Ehsaas initiative is the country’s flagship social protection program. Financial inclusion, access to digital services and economic empowerment are key areas of focus within this program.

These are noble goals, but they do cost money. The budget for the Ehsaas Emergency Cash Program was approximately $1.2 billion (PKR 203 billion) (Dawn, 2020). This one social program represents approximately 3% of the $36 billion (PKR 6.2 trillion) total revenues collected by the country in 2020 (Trading Economics, n.d.). Total government spending is significantly higher than revenues collected resulting in a growing yet necessary government debt to make up the difference. Over time, a developing nation like Pakistan will find it difficult to fund large social programs without continual assistance from the IMF and other foreign lenders.

A small investment in the Bitcoin ecosystem can yield far-reaching benefits. As we previously pointed out, appreciating bitcoin sovereign reserves can help finance some of these programs. Bitcoin may soon reach global acceptance as a pristine store of value. In this case, any nation holding a material value of this asset would be looked upon as an attractive borrower in the eyes of international lending institutions.

Perhaps the bigger play for the country lies in building out the cryptocurrency economy at the grassroots level. This initiative requires time and effort but will lead to sustainable benefits in the long run. Blockchain and smart contract software developers are on their way to becoming prized assets in this new decade of cryptocurrency. Pakistani youth need to be in a position to seize these employment opportunities. Stacks’ launch in Pakistan could not have been timed better. An excellent platform to onboard the next generation of Clarity coders from all strata of society (Clarity is the programming language used to write smart contracts for the Stacks 2.0 blockchain). This momentum should be carried forward to Solidity programming as well that is used on the Ethereum blockchain.

In a post–COVID-19 world, remote work is the new normal. Corporate America is fast becoming comfortable with employees operating from their homes located across state boundaries. The winds of change could likely push these boundaries across international borders and major oceans. The success of Remotebase, a Pakistani startup connecting Pakistani engineering teams with global companies, is proof of this concept. We may not be too far from a future state where the best candidates for the role are recruited, regardless of their physical location. Pakistan needs to identify and train its talent to be ready for these future employment opportunities.

In summary, the cryptocurrency economy has the ability to raise masses out of poverty. Government investment toward this skills upgrade and setting up basic infrastructure will be returned to the economy in the form of budding entrepreneurs, developers and product managers. All productive citizens will boost the local economy from their earnings and contribute to the tax base. In absence of this ecosystem, how else can Pakistan provide mass employment opportunities for its citizens? The time to act is now.

V. Wealth GenerationRetail Pakistani investors have a myriad of investment options available. Real estate is clearly the favored asset of choice. Within real estate, there exist residential, commercial and agricultural categories. Many investors also take advantage of high-yielding, fixed deposits and government bonds on offer in the country. Further down the list is the Pakistan Stock Exchange where less than 0.02% of the country’s population are considered active investors.

Although investment options are plentiful, the challenge is that they are all domestic in nature. As a result, investors’ overall return expectations are largely linked to the local economy’s future performance. Few investors possess the capital required to invest in real estate outside the country. An even smaller number have access to U.S. and global equities due to local capital controls along with strict KYC/AML/ATF compliance procedures of foreign financial institutions. As a result, most Pakistanis miss out on standout investment returns that are uncorrelated to the local economy.

Bitcoin fixes this unfair treatment. Using the internet and a smartphone, here lies an opportunity for the average Pakistani investor to plug into the world’s best performing asset over the past decade. The ability to participate in the returns generated from this global asset of choice will be a huge win for the country. First off, these unmatched returns will be able to provide prosperity across a large segment of the population. Secondly, this influx of cash will provide a boost to the local economy in the form of additional demand from these newly prosperous households. Finally, the capital gains earned by investors will generate additional tax revenue for the government that can be used for expanded social programs.

Detractors of bitcoin point to its volatile price performance since inception. There is no doubt that bitcoin is a volatile asset class with regular price fluctuations. However, looking at volatility alone gives you half the picture. A better way to account for these price swings would be to look at bitcoin’s Sharpe Ratio relative to other asset classes. The Sharpe Ratio measures the average return earned in excess of the risk-free rate per unit of volatility. As Chart 2 indicates, bitcoin’s Sharpe Ratio is consistently higher relative to other asset classes.

Chart 2. Bitcoin Risk Adjusted Returns versus Other Assets.We suggest the State Bank of Pakistan and securities regulators open up access to this asset class for all Pakistani investors. The ramps connecting the Bitcoin ecosystem and traditional financial institutions should be low cost and frictionless. A fully regulated national cryptocurrency exchange should be introduced with incentives to entice domestic participation. For investors not keen on purchasing bitcoin directly through an exchange, other options should be made available. For example, the introduction of a bitcoin ETF trading on the Pakistan Stock Exchange would be an attractive investment for local stock market investors desperate for diversified exposure. Finally, existing mutual funds, pension plans and insurance companies should be provided the freedom to convert a small portion of their treasuries to bitcoin. A significant percentage of the country’s population has investment exposure to these large institutions. These citizens indirectly stand to benefit from the eventual appreciation of this asset.

VI. Bitcoin MiningChina’s recent cryptocurrency crackdown has been front and center in the news. A recent statement from the People’s Bank of China, the country’s central bank, warned institutions not to provide other services related to virtual currency (Sigalos, July 2021). State-backed financial associations have warned their members to stay clear of any financing activities related to popular cryptocurrencies. They stated that any activity related to the exchange of fiat money for cryptocurrencies, providing intermediary services to facilitate trading, or conducting token-based derivatives trading, could be charged as a criminal offense in China (Feng, 2021). Furthermore, news reports from July 2021 confirmed China has shut down bitcoin miners operating in the country. This is a significant event in the Bitcoin ecosystem. Past estimates have shown as high as 65% of global bitcoin mining happened in China (Sigalos, June 2021).

Chart 3. Bitcoin Network Computing Power, one-year time frame.Chart 3 shows the impact of the Chinese mining crackdown on the total computing power supporting the Bitcoin blockchain. As miners based in China were shut down, the total hash rate powering the network fell to a one-year low. A decline in hash rate means the network is less resilient in countering attacks against the blockchain. However, it does create a boon for the remaining miners in the ecosystem as it becomes relatively easier to settle transactions and earn bitcoin rewards.

The now-defunct Chinese miners are in the process of either relocating their operations to another jurisdiction or selling their mining equipment in the secondary market at reduced prices (Reuters, 2021). At some point, this lost hashing power will return to the Bitcoin network.

How does Pakistan figure into this conversation you may ask? First, let us briefly understand the major cost drivers behind a bitcoin mining operation. First off, an internet connection is required to connect the mining operation to the network. This should be simple enough to find in the country and not pose a material burden. Next, a large miner would deploy up-front capital to purchase mining hardware, such as the Bitmain Antminer S19 or S19 Pro, which can cost $6,000–$10,000 per unit, generating approximately 100 terahashes per second (TH/s) of computing power (Cannon, 2021). Finally, and perhaps most importantly, the cost of electricity to power the mining operation is a significant recurring cost.

The shutdown of Chinese miners has resulted in secondhand mining equipment flooding the market at considerably reduced prices. This excess supply should help ease the initial capital expenditure requirement to set up the mining farm. This timing works well for anyone looking to build out a new mining operation.

The electricity cost is where things start to get interesting. Pakistan finds itself in a historically rare situation. For the first time in decades, the country has more electricity generating capacity than the local demand (Reuters, 2021). The Indicative Generation Capacity Expansion Plan (IGCEP 2021–2030) published by the National Electric Power Regulatory Authority (NEPRA) corroborates this statement. As per the report, the total installed generation capacity in the country reached 34,501 MW as of May 2021. Peak demand in the country during 2019–2020 was 22,696 MW (recorded during September 2019), while the lowest demand was 5,635 MW (recorded during January 2020) (National Transmission and Dispatch Company, 2021).

OK, availability of excess electricity and supply over demand is a good start. What about the cost to generate this additional electricity? Pakistan’s power purchase agreements with its independent power producers are mostly take or pay contracts. This contractually binds the government to make capacity payments for the excess electric generation capacity, whether it is used or not. In essence, we can classify this already incurred electricity payment as a sunk cost and ignore it in our mining cost-benefit analysis.

It is our suggestion that the federal government take advantage of this situation. Excess electricity supply coupled with an expense that is already budgeted is too good to pass up. Moreover, the recent reduction in the network’s hash rate makes it economically attractive to begin mining operations immediately. Bitcoin mining farms should be set up near power plants to minimize any transmission losses. Used mining equipment provides a cost-effective means of getting started. Finally, the government can choose to maximize the mining farm output in winter months when local demand is relatively low. If bitcoin prices continue to rise as per our expectations, this would be another avenue for the federal government to generate massive revenues. According to a recent news article in Dawn, “If Pakistan uses this energy for bitcoin mining using the latest S19 Pro Antminer (assuming 10,000MW of excess energy available at a cost of $0.12 per kW/hour), it can generate $35 billion worth of Bitcoin per year at current valuations. Simply put, this means we can pay off our external debt in two years” (Khwaja, 2021).

VII. RemittancesThe State Bank of Pakistan has prioritized the rollout of Raast. These financial rails will enable low-cost, real-time payment and settlement across government institutions, banks, merchants and individuals. Additionally, this initiative will make it possible for millions of unbanked citizens to enter the digital financial economy, simply by using a smartphone. This infrastructure will serve as a backbone of the local digital economy with the capability for fintech firms to build Layer 2 applications. All evidence points to a flourishing local remittance ecosystem.

The next major challenge lies in tackling the network of international remittances coming into the country. In fiscal year 2020–2021, the amount sent home by overseas Pakistanis reached a historic high of $29.4 billion (Siddiqui, 2021). These valuable funds are used by the government to boost its foreign reserves, repay debt to international lenders and cover its import bill. Clearly, this source of funds is of dire importance to the effective functioning of the local economy.

However, international payment remittance is a high friction process. International wire transfers are expensive and not suited for small remittance amounts. Service providers such as Western Union and MoneyGram do not provide real-time settlement. They introduce further obstacles as recipients need to physically travel to an authorized dealer location to pick up the funds. All in all, a clunky process.

PayPal, a global leader in online payments, allows people in more than 190 countries to send and receive money and acts as an international bank account. The fact that this payment service is not available to Pakistani residents is a travesty. The following news report aptly sums up the situation:

“In 2019, a Payoneer index reported that Pakistan has the fourth largest freelancer community in the world. In 2020, the same fintech company reported that Pakistan is the world’s eighth fastest-growing freelancing economy. Currently, there are around one million freelancers in Pakistan and yet the Pakistani freelancers have no reliable payment options … The unavailability of PayPal is hitherto the biggest plight of the Pakistani freelancer community. Almost all online job platforms have a PayPal option … the ease of user interface, timeliness and compatibility offered by PayPal makes it stand out among its competitors. Most good clients refuse to work with Pakistani sellers because they only trust PayPal for online transactions. This nullifies the proposition of a ‘domestic alternative’. PayPal’s absence is significantly felt, especially in the online working community” (Bhatti, 2021).

Bitcoin’s monetary network provides a comprehensive solution to this problem. The core blockchain network enables transfer of value across two users, regardless of their geographical location. A worldwide network of financial rails already exists within the Bitcoin ecosystem. Using a smartphone and an internet connection, a user can easily plug into this global network. The decentralized nature of this ecosystem allows participation without seeking permission. No central authority has the power to de-platform a user from this ecosystem, let alone the fifth most-populated nation in the world.

The Lightning Network is a Layer 2 payment protocol that sits on top of the core Bitcoin blockchain. This innovation allows the network to become scalable. Micropayments can be transferred on this layer on a real-time basis with minimal fees. Subsequently, the initial and final balances from Layer 2 are settled on the core blockchain. Strike, a fintech company pioneering the use of payments over the Lightning Network, is already operating in El Salvador. By allowing users to plug into the Bitcoin network, it seamlessly allows both inward international remittances along with a local payment infrastructure. Even though the Bitcoin monetary network is used, the remitter and receiver of funds never have to own any bitcoin. Volatility of bitcoin prices is not a concern due to real-time conversion of currency taking place.

We suggest the federal committee overseeing cryptocurrency should invite fintech players such as Strike to understand the benefits of this solution. Pakistan should begin work on seamlessly connecting Raast to the Bitcoin ecosystem. As previously mentioned, one way to achieve this is to introduce a State Bank–backed national cryptocurrency exchange that is connected to Raast. KYC, tax filing status and proof of funds of users can be verified upon the onboarding process. We are of the opinion that Pakistani cryptocurrency users will flock to a local solution as long as there exists a seamless ramp to enter and exit the ecosystem. Furthermore, a local exchange allows ease of oversight to regulators and tax authorities.

VIII. RisksAs with any investment, the Bitcoin ecosystem is not without risk. Our team reviews country-specific risks for Pakistan as it plans to embark on its cryptocurrency journey.

A. China

Chinese authorities have laid bare their obvious displeasure with the cryptocurrency ecosystem. China is one of the largest lenders to Pakistan and also a very strong geopolitical ally. The China–Pakistan Economic Corridor is an integral source of foreign direct investment, infrastructure development and employment in the country. Understandably, the recent action taking place against cryptocurrencies in China should be carefully considered by local policymakers.

Commentators have speculated on the possible reasons behind the crackdown in China. It would be useful to separate facts from sensational journalism to better understand China’s concerns.

B. International Monetary Fund

The IMF is also a large lender to the country. Pakistan has received 13 structural adjustment programs from the IMF since 1988 (Dawn, 2019). The organization has been critical about the role of cryptocurrencies as legal tender in a nation. Unsurprisingly, this assessment was put forward by the IMF soon after El Salvador announced its plans to adopt bitcoin as a national currency (Adrian, 2021).

Although our team does not recommend adopting bitcoin as legal tender, the criticism from another important lender should be examined carefully. One way to mitigate this risk would be to invite IMF representatives to be included when formulating the cryptocurrency strategy in the country.

C. Financial Action Task Force

Pakistan has been tirelessly working these past few years toward exiting the FATF gray list. It was recently reported that the FATF has called on the government to better regulate the cryptocurrency industry.

The government’s first response in setting up the federal committee to oversee cryptocurrency regulation is a promising one. Moreover, they have included the FATF as a member of the committee. Money laundering and terrorist financing issues will likely be top of mind for the FATF.

A flourishing and formal cryptocurrency economy in Pakistan is not possible without tackling the FATF’s concerns. Regulations to bring exchanges, dealers and users together is a win-win for all stakeholders involved. This will help bring the industry out of the shadows and lay down the foundations needed for sustainable development.

D. Capital Outflows

Market observers have speculated on several reasons behind China’s actions relating to cryptocurrencies. One of them is centered around the ease of capital flight from China through the use of cryptocurrencies.

This flight of capital is a significant risk for Pakistan as well. Admittedly, it is not entirely possible to stem the flow of capital in the cryptocurrency ecosystem. However, regulations built around the entry and exit points of the ecosystem play a role in mitigating this risk.

Furthermore, Pakistani residents will face stiff scrutiny when attempting to withdraw funds from the cryptocurrency ecosystem in any foreign jurisdiction. There exists a major incentive for domestic users to work within the regulatory framework and pay the required taxes on investment gains. That incentive being immediate transfer of cryptocurrency funds to their local bank accounts.

This is a guest post by Frontier Capitalism. Opinions expressed are entirely their own and do not necessarily reflect those of BTC Inc. or Bitcoin Magazine.

References

Ahmed, A. (2021, June 2). “KP Dissolves Advisory Committee On Cryptocurrency.” Business Recorder, https://www.brecorder.com/news/40097197.

Bhatti, N. A. (2021, May 29). “Still No PayPal.” The News, https://www.thenews.com.pk/print/841430-still-no-paypal.

Bill Miller IV, C. C. (2021, January 21). “Income Strategy 4Q 2020 Letter.” Miller Value, https://millervalue.com/4q20-income-strategy-letter/.

Cannon, M. A. (2021, August 10). “Is Bitcoin Mining Profitable or Worth it in 2021?” Buy Bitcoin Worldwide, https://www.buybitcoinworldwide.com/mining/profitability/.

CEIC. (2021, July). “Pakistan Gold Reserves,” https://www.ceicdata.com/en/indicator/pakistan/gold-reserves.

Dawn. (2020, July 17). “Ehsaas Programme Being Enhanced From Rs144bn To Rs203bn” https://www.dawn.com/news/1569458.

Farooq, U. (2021, March 18). “Pakistani Province Plans To Build Pilot Crypto Currency Mining Farms.” Reuters, https://www.reuters.com/article/us-crypto-currency-pakistan-idUSKBN2BA0KW.

Farooq, U. (2021, July 16). “Pakistan Moves To Bring Cryptocurrency Boom Out Of The Dark.” Reuters, https://www.reuters.com/technology/pakistan-moves-bring-cryptocurrency-boom-out-dark-2021-07-16/.

Feng, C. (2021, May 19). “China Sends Another Warning On Cryptocurrency Risks Amid ‘Wild Fluctuations’.” South China Morning Post, https://www.scmp.com/tech/policy/article/3133967/beijing-sends-another-warning-cryptocurrency-risks-amid-recent-elon.

Frankenfield, J. (2020, June 30). “Double Spending.” Investopedia, https://www.investopedia.com/terms/d/doublespending.asp.

Ikram, T. (2021, January 14). “What Is Raast? And How Will It Help An Everyday Pakistani?” TechJuice, https://www.techjuice.pk/what-is-raast-and-how-will-it-help-an-everyday-pakistani/.

Khurshid, J. (2020, December 19). “State Bank Did Not Declare Crypto Currency Illegal, Shc Told.” The News, https://www.thenews.com.pk/print/760929-state-bank-did-not-declare-crypto-currency-illegal-shc-told.

Khwaja, A. F. (2021, March 1). “Bitcoin Mining: A Solution To Pakistan’s New Energy Problem?” Dawn, https://www.dawn.com/news/1609742.

LUMS. (2021, February 16). “Bringing Blockchain Technology to the Forefront: LUMS To Leverage Stacks Grant To Build Novel Academic Programme in Pakistan.” LUMS, https://lums.edu.pk/news/bringing-blockchain-technology-forefront-lums-leverage-stacks-grant-build-novel-academic.

MicroStrategy. (n.d.). “Bitcoin for Corporations.” MicroStrategy, https://www.microstrategy.com/en/bitcoin/bitcoin-for-corporations.

National Transmission and Dispatch Company, Pakistan. (2021). The Indicative Generation Capacity Expansion Plan (IGCEP 2021–2030). National Electric Power Regulatory Authority (NEPRA) .

Reuters. (2021, June 24). “China’s Bitmain Suspends Sales Of Cryptomining Machines After Beijing’s Mining Ban,” https://www.reuters.com/business/chinas-bitmain-suspends-sales-cryptomining-machines-after-beijings-mining-ban-2021-06-25/.

Reuters. (2021, February 25). “Pakistan’s Unexpected Dilemma: Too Much Electricity,” https://www.dawn.com/news/1609241.

Siddiqui, S. (2021, July 13). “Remittances Soar To All-time High In FY21.” The Express Tribune, https://tribune.com.pk/story/2310273/remittances-soar-to-all-time-high-in-fy21.

Sigalos, M. (2021, June 15). “China Is Kicking Out More Than Half The World’s Bitcoin Miners — And A Whole Lot Of Them Could Be Headed To Texas.” CNBC, https://www.cnbc.com/2021/06/15/chinas-bitcoin-miner-exodus-.html.

Sigalos, M. (2021, July 7). “China’s War On Bitcoin Just Hit A New Level With Its Latest Crypto Crackdown.” CNBC, https://www.cnbc.com/2021/07/06/china-cracks-down-on-crypto-related-services-in-ongoing-war-on-bitcoin.html.

The Express Tribune. (2020, December 6). K-P Assembly Passes Resolution To Legalise Cryptocurrency, https://tribune.com.pk/story/2274888/k-p-assembly-passes-resolution-to-legalise-cryptocurrency.

Trading Economics. (n.d.). “Pakistan Government Revenues,” https://tradingeconomics.com/pakistan/government-revenues#:~:text=Government%20Revenues%20in%20Pakistan%20is,according%20to%20our%20econometric%20models.

US Inflation Calculator. (2021, August 11). https://www.usinflationcalculator.com/.

World Gold Council. (2021, September 1). “Gold Hub.” World Gold Council, https://www.gold.org/goldhub/data/monthly-central-bank-statistics.

Yahoo Finance. (2021, September 1). “Top Cryptos by Volume (All Currencies, 24hr),” https://finance.yahoo.com/u/yahoo-finance/watchlists/crypto-top-volume-24hr/?guccounter=1.

Why this matters

This bitcoin story adds another data point to the current market tape and is useful when read alongside nearby source coverage.

Original source

Read on Bitcoin MagazineRelated market context

CLARITY Act splits Wall Street and crypto as Goldman Sachs breaks with banks and Charles Hoskinson backs Warren

The revised CLARITY Act is exposing unusual divisions across Wall Street, Washington and the crypto industry as lawmakers struggle...

Poolin, Once-Dominant Bitcoin Mining Giant, Announced Bankruptcy

Key Takeaways: Poolin has filed for Chapter 11 bankruptcy protection in the U.S., representing about 20% of Bitcoin’s global hashr...

Poolin Files Chapter 11 As Bitcoin Miner Moves Toward $52M Asset Sale

Poolin Technology has filed for Chapter 11 bankruptcy protection, setting up an orderly wind-down and asset sale process tied to i...

Poolin, Once One of Bitcoin's Biggest Mining Pools, Files for Bankruptcy

The Singapore-based pool never recovered from freezing withdrawals in 2022. Now it's auctioning off its last Texas mining sites to...

Morgan Stanley Bitcoin ETF Nearly Notches $400M in Assets

Bitcoin Magazine Morgan Stanley Bitcoin ETF Nearly Notches $400M in Assets Wall Street giant Morgan Stanley Bitcoin exchange-trade...

Samsung Says Wallet Will Add Stablecoin Support

Samsung Wallet will support stablecoins, Samsung product manager Lee Dinham said at the company's Galaxy Unpacked event in London...