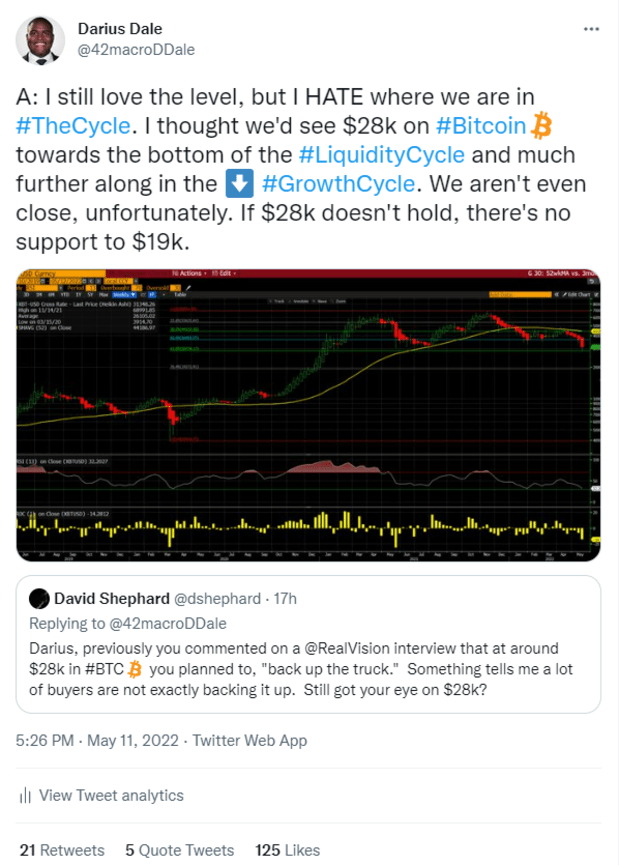

Current Bitcoin Price Action: A Macro View

Risk assets continue to face a challenging environment as Federal Reserve officials take incremental actions to tighten financial conditions.Darius Dale is the Founder and CEO of 42 Macro, an investment research firm tha...

Risk assets continue to face a challenging environment as Federal Reserve officials take incremental actions to tighten financial conditions.

Darius Dale is the Founder and CEO of 42 Macro, an investment research firm that aims to disrupt the financial services industry by democratizing institutional-grade macro risk management processes.

Key TakeawaysShort-Term (less than one month): Our market signaling process is pointing to a continuation of the challenging environment for risk assets. While a downside surprise in the U.S. April CPI data provided some reprieve, we, at 42 Macro, don’t think a grossly anticipated negative rate of change inflection will do much in isolation to catalyze a durable bottom in either stocks or bonds given our analysis of second-round inflation momentum and the latest forward guidance out of the Federal Reserve and European Central Bank.

Medium-Term (three to six months): We continue to see downside risk to around $3,200–$3,400 for a durable bottom in the S&P 500 — which would likely catalyze another 30–50% decline in bitcoin once cross-asset correlation risk kicks in. While that range may prove to be 200–300 points too low once the Fed put option is factored in, we do believe it is important for every investor to comprehend the risk we continue to see on an ex ante basis.

(Source)Our base case scenario sees the U.S. economy returning to inflation in April 2022 and May after a brief stint in reflation before settling into a persistent deflation by June. Inflation and deflation are the two components of 42 Macro’s “GRID Regimes” that feature elevated volatility and covariance across asset classes. Given this condition of elevated portfolio risk, it is likely we are only in the middle innings of the bear market(s) in high-beta risk assets we have been anticipating since the fall.

(Chart by 42 Macro)With the Fed unlikely to receive any signals from either the labor market or inflation statistics to stop tightening monetary policy for at least another quarter (perhaps two or three), it is likely financial conditions must tighten considerably to force a dovish pivot. While U.S. and global growth dynamics do not yet support such an adverse outcome, we believe simultaneous deteriorations in the liquidity cycle, growth cycle and profits cycle will continue to perpetuate a protracted and pervasive breakdown in risk appetite.

(Graph by 42 Macro) (Graph by 42 Macro)The balance of risks surrounding our model outcome are balanced. With respect to what we believe is a low-probability bull case, risk inflation peaks and slows much faster over the next two to three months than we, economist consensus and the Fed, currently anticipate, leading to a sharp repricing lower of the projected path for the Fed Funds Rate in money markets. Any such sharp deceleration in inflation would also inflate real incomes and delay a more meaningful slowdown in growth by perpetuating a growth plus inflation (“Goldilocks”) soft landing in the U.S. and across large parts of the global economy. Goldilocks is an extremely bullish regime for bitcoin, with an annualized expected return north of 400%.

(Graph by 42 Macro)With respect to what we believe is a low-probability bear case, a deterioration on the geopolitical front amid incremental supply chain disruptions stemming from China’s “Zero COVID” policy may sustain the ongoing inflation impulse for another two or three months. This causes Fed officials to take incremental actions (relative to market pricing) to tighten financial conditions into the teeth of the sharper deceleration in growth our models have persisted throughout 2H22E. The resulting deflation would likely be deeper and more protracted, perpetuating jump conditions in recession probability models. A deep deflation — as evidenced by a (two-sigma) growth delta is quite bad for bitcoin. That regime features a negative 64% annualized expected return for the digital asset.

This is a guest post by Darius Dale. Opinions expressed are entirely their own and do not necessarily reflect those of BTC Inc. or Bitcoin Magazine.

Original source

Read on Bitcoin MagazineRelated market context

Bitcoin price faces new risk as big buyers lose conviction

Bitcoin’s largest buyers are no longer behaving like a reliable backstop for the largest cryptocurrency. The exchange-traded funds...

Bitcoin price challenges $64,000 weekend wall – needing a breakout or risk a deeper correction

Bitcoin reclaimed $64,000 on June 12 and touched an intraday high of $64,301 in the same session that spot ETF flows finally flipp...

Jason Yanowitz: Transparency and trust are vital for crypto growth, tokenization is reshaping financial markets, and regulation is necessary for industry maturity | Bell Curve

Tokenizing assets could revolutionize financial markets by bringing infrastructure on-chain and enhancing transparency. The post J...

Bitcoin faces one of its biggest mining difficulty drops as miner margins collapse

The Bitcoin network is poised to execute one of the largest downward adjustments to its mining difficulty in its 17-year history t...

Standard Chartered Says Bitcoin Bottomed Near $59,000 As Crypto Winter Ends

TL;DR Standard Chartered’s Geoffrey Kendrick reportedly says Bitcoin’s $59,000 area marked the cycle bottom. The note cites SpaceX...

Coinbase Quantum Report Warns Millions Of Bitcoin Could Face Future Security Risks

TL;DR Coinbase’s Quantum Advisory Council published a report on post-quantum migration and abandoned coins. The report estimates t...