House Democrats Want to Close Crypto Tax Loophole

Congressional Democrats have been talking about their $3.5 trillion, 10-year spending package even before the ink was dry on the $1 trillion infrastructure package pending before the House. We're getting our first glimps...

Archive context

Older archive item. Useful for background and entity history, but not a fresh market-moving signal.

Congressional Democrats have been talking about their $3.5 trillion, 10-year spending package even before the ink was dry on the $1 trillion infrastructure package pending before the House.

We're getting our first glimpse of how they plan to pay for their projects, which cover everything from healthcare to climate change. As with the infrastructure package, they believe there's money to be raised from cryptocurrency.

House Democrats are proposing that $2 trillion of the money needed should come from tax increases, with a projected $16 billion ($1.6 billion per year) derived from adding cryptocurrencies and other assets to the wash-sale rule.

If you've ever used or sold cryptocurrencies in the U.S., you're likely aware that these count as taxable events. If the Bitcoin, Ethereum, or other cryptocurrency you cash out has been in your wallet for more than a year, those earnings are taxed at a long-term capital gains tax rate. If you've had it for less than a year, you get taxed at the short-term rate, which is higher. By the same token, so to speak, if your portfolio loses value, you can claim a loss and earn a deduction on your taxes.

But what if you sell some crypto, watch the price drop and buy it back for less? Right now, the Internal Revenue Service doesn't have any tools to mitigate this practice, which, when done in large volumes, can manipulate the price.

In the world of traditional finance, however, stock traders would have to wait 30 days before re-buying an asset if they wanted to claim a capital gains deduction. Cryptocurrency, classified as a property by the IRS, has no such limitations. Crypto users can cash out, get the deduction, then immediately re-buy at a lower, more favorable price.

For now.

The House proposal, if accepted, would treat crypto like stocks in this regard.

IRS Won't Go After Bitcoin Miners Regardless of ‘Broker’ Definition: ReportsBoth Coin Center and the Blockchain Association have signaled that the proposal isn't unreasonable, let alone an existential threat—unlike the proposal within the Senate infrastructure bill to make crypto actors beholden to tax reporting requirements. They argued that mandating crypto miners, validators, wallet providers, and blockchain app developers to file 1099 forms for the millions of anonymous people transacting via blockchains was unworkable and could chill American innovation in the crypto sector—though the Biden administration has reportedly said it wouldn't apply the law to non-custodial actors, such as cryptocurrency miners and software developers.

That bill, which passed on a bipartisan vote in the Senate, is now before the House, which is expected to pass without amendment.

Why this matters

This cryptocurrency story adds another data point to the current market tape and is useful when read alongside nearby source coverage.

Original source

Read on DecryptRelated market context

Bitcoin Miners Are Becoming AI Landlords. But Which Leases Are a Positive Investment Signal?

The best story in bitcoin mining hasn’t had anything to do with bitcoin in a long time. Years ago, this business (which long lived...

$7 Trillion Investment Giant Fidelity Backs New Crypto Clarity Act

Bitcoin Magazine $7 Trillion Investment Giant Fidelity Backs New Crypto Clarity Act Investment giant Fidelity is the latest big pl...

Bitcoin News: Johor Syndicate Cleared $25,000 Monthly by Stealing Power

In Bitcoin news today, police in Malaysia dismantled a Bitcoin mining syndicate following four raids on July 22 and 23 by Tenaga N...

BitMEX Shuts Down After 11 Years as Arthur Hayes Bids Farewell and CZ Reflects on Crypto Exchange’s Legacy

The exchange announced on July 23 that it will permanently cease operations at 04:00 UTC on September 23, 2026, following a strate...

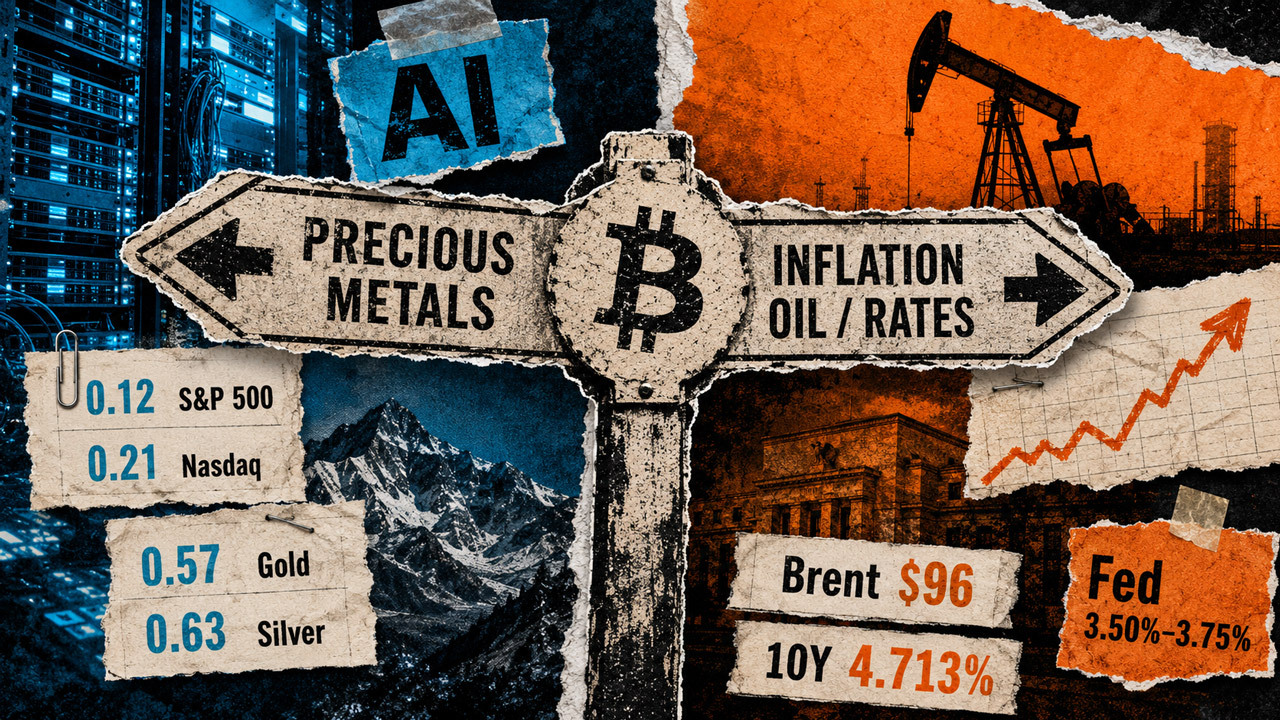

Bitcoin broke away from AI stocks but now $96 oil could turn its escape into a trap

Bitcoin's daily correlation with the S&P 500 fell to 0.12 during the second quarter, down from 0.58 in the fourth quarter of 2025,...

Strategy now publishes the Bitcoin return threshold below which it may have to restructure

Strategy’s newly published metric shows Bitcoin could decline at a constant annual rate of 11.34% across the weighted duration of...